Morgan DeFoort

Jul 30, 2019

Tags: Impact Investing,

View More Insights

Catalytic Investing in Emerging Markets

Catalytic Investing in Emerging Markets The Nexus of Agriculture and Energy in Africa: Five Lessons for Bridging the Ag-Energy Gap

The Nexus of Agriculture and Energy in Africa: Five Lessons for Bridging the Ag-Energy Gap Looking Beyond Appliances: Systemic Barriers to Minigrid Demand Stimulation

Looking Beyond Appliances: Systemic Barriers to Minigrid Demand Stimulation The Clock is Ticking on Energy Access: Exploring Factor[e] Ventures’ Big Bet on Mini-Grids

The Clock is Ticking on Energy Access: Exploring Factor[e] Ventures’ Big Bet on Mini-GridsImpact Metrics… Strategy or Storytelling?

As early-stage impact investors, we at Factor[e] Ventures are often asked how we measure an investment’s impact. What are the metrics that we use? How can we determine if a venture is worthy of the limited risk capital available in the impact sector? Can an investment start out as high-impact and then stray from the mission? We’d like to argue that looking at metrics after the fact is likely the least effective way to answer these questions, and that, in fact, the best way to measure impact is to start by understanding an investor’s intention.

At our core, Factor[e] is a problem-focused investor. We constantly ask, “Is there a scalable, venture-backable solution Y to a social problem X?” This approach requires understanding problems in our target markets, understanding the range of possible solutions, and having a theory about how these might intersect. This theory — this thesis — drives how we think about impact and who we invest in.

It’s important to note that true thesis investing is quite different than thematic investing [1]. Thematic investing is about identifying big trends and then making bets in those spaces. Thesis investing instead relies on a specific view of how a space could change and — rather than just anticipating those changes — investing in a way that will instigate and accelerate that sectoral disruption. Themes are static: a theme emerges, matures, and then mainstreams. A thesis is dynamic: constantly evolving to incorporate new data from the market, new technologies on the horizon, and shifting to stay in front of a sector.

This approach demands organizational compatibility and discipline. Everyone in the organization must buy into the thesis, and investment decisions must be measured against that thesis via a documented process. When the thesis is directionally correct, and executed well, the approach will have transformative impact in a sector — and can produce the best possible returns in that sector. In fact, the data show that when this strategic approach is applied, a positive correlation between impact and financial return [2] will exist, the implications of which deserve to be examined — especially as we look to measure impact.

What is an Impact Investment Really?

The IESE Business School and the Family Office Circle Foundation (Grabenwarter et al) conducted interviews with over 60 dedicated impact investors to better define impact investing, understand traits of success and failure, and explore “the popular assumption that impact investing involves a trade-off between financial gain and social impact” [3]. The group developed five requirements to define an impact investment.

The first requirement is a profit orientation, which should be both obvious and non-controversial. Less obvious is the second requirement: “that there exists a positive correlation between impact and financial return, where the financial return drivers of the funded businesses cannot be dissociated from the impact objectives”. The authors of the study argue, “If the business model is the means of achieving the impact objective, by definition there has to be a positive correlation between the impact objectives and the business model’s financial return. Any business model in which every unit of social/environmental impact has a cost in terms of financial return is therefore inevitably a disguised form of philanthropy.” This requirement has important implications for investors when it comes to making investment decisions, as well as monitoring the impact of those investments. The last three requirements are that impact is intentional, measurable, and has a positive effect on society.

Impact Investing: Making to Measuring

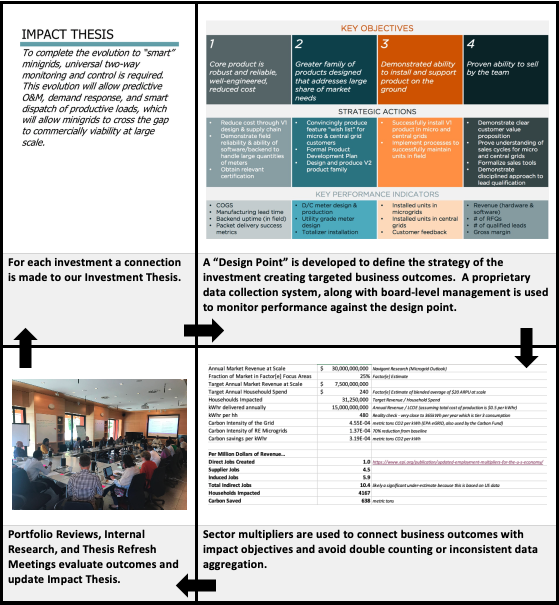

The requirements above highlight the importance of an investment thesis not just in guiding investment decisions but in navigating the entire process — including measurement. Impact investing is a long chain of anticipated events subject to all the normal chaos associated with entrepreneurship and then compounded by our expectations of sector impact. The one element that can be carefully controlled in the process is our thesis. Thus for Factor[e], all of the decisions we make from beginning to end are linked to our thesis. Before an investment is made, the strength of alignment between our thesis and the venture is tested — specifically, we ask whether the natural outputs of the business will result in outcomes that will positively impact the sector. If we are confident that our thesis connects potential outcomes with impact, we satisfy ourselves that our investment 1) is intentional and 2) will have positive social impact correlated to financial return. This dramatically simplifies and clarifies impact measurement. As an organization, we can focus on more traditional and tangible financial and operational metrics as proxies for impact, relying on the logic of our thesis to ensure that the relationship between financial success and impact is sound.

For example, several years ago we identified smart metering as a critical need in the mini-grid sector while developing our Access to Energy Thesis. We knew that improved access to electricity via microgrids was the lowest-cost approach to energy delivery (especially for the rural poor), benefiting economic growth while reducing carbon emissions. But there’s a big leap from “mini-grids” as an investment theme to focusing on a single piece of hardware (in this case, smart meters). The thesis development process began by understanding the detailed technical and economic challenges of operating a mini-grid. We built models and we ran the numbers. We talked to operators. We talked to the customers of those operators. It’s not enough to know that mini-grids are cheaper than grid extension — we had to also understand what the main cost drivers for mini-grids were, not just from a first-cost perspective, but also from an operational perspective. The current thinking at the time was that smart meters were an unnecessary luxury, but looking at the numbers, we saw a different story. We saw that smart meters with two-way communication enabled mobile money payments, automated meter reading, theft detection, and remote demand management. The operational savings far exceeded the investment cost, moving projects in our target markets closer to commercial viability. Satisfied with our thesis, we landscaped every smart-metering technology on the market and ultimately became one of the first investors in SparkMeter.

So how do we measure the impact of that investment? A smart meter does not deliver electricity alone — we can’t show our investment committees photos of kids studying by the light of a smart meter. So how do you judge the impact of a technology that is broadly enabling? This is the value of a thesis as a foundation when evaluating impact. The more meters SparkMeter sells, the more evidence there is that they are providing a good value to the sector — helping the whole sector achieve scale. Per our earlier discussion, we see that a positive correlation exists between the impact and financial performance of the venture. We know from our thesis development work that the mini-grid market should reach $30B in annual revenue at scale [4], which will result in a carbon savings of 5 million metric tons per year [5]. We also know that in developed economies the energy sector produces 10 jobs per $1M in revenue [6] and that there is a strong correlation between primary energy consumption and GDP per capita, as well as HDI (human development index) scores. We can now focus on maximizing revenues of our smart meter investment, and supporting the venture to scale, knowing that we can easily measure financial and operational metrics (funding raised, headcount, revenues) which lead (by years) the eventual lagging indicators of carbon reductions, lives impacted, and customers who gain access — and tie those revenues back to impact through simple multipliers. It’s not as easy as showing photos of kids studying, but it is based in sound logic and rooted in an understanding of what will move the market toward universal energy access.

Testing Thesis as a Basis for Impact Measurement

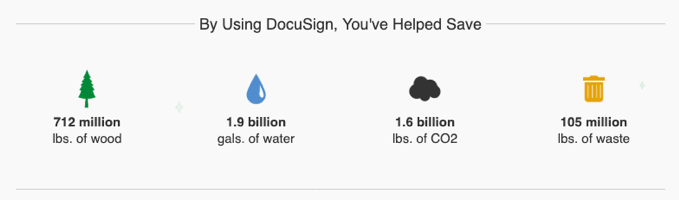

DocuSign®, which debuted on the NASDAQ in April of 2018, is a software company that enables the distribution and signing of agreements online. According to the company, the software has prevented over 1.6 billion pounds of carbon dioxide emissions and has saved 712 million pounds of wood [6]. So is DocuSign® an impact investment? At Factor[e] we would argue that it is not — even though there are tangible, measurable (and impressive) impact metrics reported.

Why not? The founders of DocuSign did not create the company as a way to save trees or carbon, and Scale Ventures certainly didn’t invest against a carbon impact thesis when they led a $27 million round in 2010. The example falls short due to the lack of intentionality. While the metrics are impressive, the impact is a byproduct of the company — this in no way discounts the environmental benefit, but from an impact investmentperspective the lack of thesis means the investment’s impact was not deliberate. Impact investments that rely on good things happening regardless of the strategy employed can be reduced to either luck or good storytelling after the fact — neither of which require the time and effort of an impact-focused investment management team. Going back to Grabenwarter, “Defining such a change theory implies defining an expected impact when the investment is decided upon. Defining an expected impact result that show a causal link between the investment made and the result achieved is actually more vital as a criterion for impact investing than the actual methodology or type of impact metrics used.”

An Important Addendum: Our Meta-Thesis

Turning the lens away from our specific investment areas, e.g. Access to Electricity, it can also be helpful to examine the way we operate generally. The challenges we tackle as impact investors have immediacy to them: climate change is accelerating, while limited access to economic participation threatens food security, education, health, and social cohesion. We must push for scale and impact quickly. How do we respond as impact investors in a way that balances the need for rapid growth/impact with realities of investment time-cycles?

Working with these realities ever present has informed our meta-thesis — lessons learned or reinforced in our journey thus far. Our lodestar is creating the conditions for economic vibrancy faster, better, cheaper, and, critically, with greater resource efficiency and more inclusively than so-called developed countries. This leads us to:

- Invest in core infrastructure for driving economic growth and poverty alleviation: access to energy, agriculture, waste and sanitation, and sustainable mobility.

- Invest along the value chain — rarely in the markets we work in are there venture opportunities that operate without the need for “fixing” other areas of a broken value chain.

- Work in-market, close to our ventures and their customers.

- Be very, very hands on. It’s not enough to pick the right teams and technologies without also investing in their difficult journey into the market. There must be support beyond funding. To responsibly invest in these sectors means bringing the ability, aptitude, and willingness to throw everything you can into the success of the venture, balanced by the discipline and rigor of a commercial investor.

- Embrace technology risk wherever appropriate to moving our theses and focus areas forward.

- Operate with the rigor and mindset of a commercial investor — so that commercial capital will be willing to follow-on invest (there is not enough philanthropic capital in the world to solve these challenges without leveraging commercial capital).

This meta-thesis and individual investment theses are paired with “convictions” that we have developed about our focus areas. For example, we believe that the world is moving toward (and has to move toward) renewable mini-grids for a large share of the rural electrification challenge/opportunity and that the mini-grid sector doesn’t yet have the tools and enabling layers to deliver on that promise (that’s the opportunity for investment). We believe that you can’t “disrupt” the farming landscape inclusive of smallholder farmers in tropical agricultural contexts without “doing too much.” You need to bring more of the value chain and solution to your customers who generally lack physical and financial access to solutions that already exist and are being developed. If you’re not delivering a full-stack solution, you’ll either not get off the ground or you’ll only serve larger and more prosperous farmers.

Commitment to Intentional, Thesis-Driven Impact Investment

The learnings and convictions that make up our thesis-based approach are not static or developed in isolation. We believe impact investing is a partnership not just with the portfolio but also those who invest through us. We actively engage our investors in the refinement and execution of our thesis — perhaps the best way to ensure alignment of purpose. We accept the high expectations of our investors, and they graciously give us the freedom to test our thesis in return. It is a partnership that has yielded notable early results and we hope is another mechanism for creating impact the sector.

At the end of the day, measuring impact requires understanding intentions. Capturing those intentions in a thesis can be intimidating; we’re certainly not always right- and documenting a thesis for funders and our investing peers to later judge has risk, but no more than that which the entrepreneurs we are betting on face daily. Measuring the effectiveness of a thesis may also not be as tidy a reporting carbon saved, or electrons delivered — but for early stage impact investors we believe it is the measure by which investors should be judged.

References

[1] Fred Wilson, “Thematic vs Thesis Driven Investing” https://avc.com/2009/11/thematic-vs-thesis-driven-investing/[2] Uli Grabenwarter, Heinrich Liechtenstein, “In search of gamma, an unconventional perspective on impact investing” IESE Business School & Family Office Circle Foundation. https://www.impactstrategist.com/wp-content/uploads/2015/12/In-search-of-Gamma.pdf[3] Navigent Research https://microgridknowledge.com/microgrid-market-navigant/[4] Factor[e] calculation using data from EPA eGRID[5] Economic Policy Institute 2019[6] Based on the last time I used DocuSign®